- First-time buyers purchasing a new-build home can receive up to €30,000 back from Revenue under the Help to Buy scheme

- The rebate is 10% of the purchase price, capped at €30,000, and is funded by income tax and DIRT you paid over the past four years

- The scheme applies to new-build homes only — not second-hand properties — and the home must be your primary residence

Buying your first home in Ireland is a significant financial undertaking. The Help to Buy (HTB) scheme is one of the most generous tax incentives available to first-time buyers — a cash rebate of up to €30,000 funded by income tax and DIRT you've already paid. Despite the benefit, many first-time buyers don't fully understand how the scheme works or don't claim the maximum amount available to them. This guide covers everything you need to know.

What Is the Help to Buy Scheme?

The Help to Buy scheme allows first-time buyers to claim a rebate of 10% of the purchase price of a new-build home, up to a maximum of €30,000. The rebate is drawn from income tax (including PAYE) and Deposit Interest Retention Tax (DIRT) that you've paid over the four tax years before your application.

The scheme was introduced in 2017 and has been extended multiple times. As of 2025, it is scheduled to run until 31 December 2029, giving first-time buyers certainty to plan around it.

Who Qualifies for Help to Buy?

To be eligible, you must meet all of the following conditions:

- You are a first-time buyer — you have never previously owned a residential property in Ireland or abroad

- You are purchasing a new-build home (built by a Revenue-approved contractor), or building a self-build property

- The property value is €500,000 or less

- You are taking out a qualifying mortgage — at least 70% of the purchase price must be funded by a mortgage from a qualifying lender

- The home will be your principal private residence — you must live in it for the first five years

- All buyers on the mortgage must be first-time buyers (so you can't buy with someone who has previously owned a home)

Second-hand properties do not qualify. This is the single most common misunderstanding about the scheme. The HTB is specifically aimed at increasing new housing supply.

How Much Can You Claim?

The rebate is 10% of the purchase price, capped at €30,000 in total. To receive the full €30,000, the property must cost at least €300,000.

| Purchase Price | HTB Rebate (10%) | Maximum Capped At |

|---|---|---|

| €200,000 | €20,000 | €20,000 |

| €250,000 | €25,000 | €25,000 |

| €300,000 | €30,000 | €30,000 (cap) |

| €450,000 | €45,000 | €30,000 (cap) |

The rebate is also limited to the total income tax and DIRT you paid in the four years before your application. If you paid only €15,000 in qualifying tax over four years, your maximum rebate is €15,000 regardless of the property price.

How Is It Calculated? A Worked Example

Liam and Sarah, first-time buyers, buying a new build for €380,000 in 2025

| Amount | |

|---|---|

| Purchase price | €380,000 |

| HTB at 10% | €38,000 |

| Cap applies | €30,000 |

| Liam's income tax paid (2021–2024) | €28,000 |

| Sarah's income tax paid (2021–2024) | €24,000 |

| Combined tax paid | €52,000 |

| HTB Rebate Payable | €30,000 |

Their combined tax paid (€52,000) exceeds the cap (€30,000), so they receive the full €30,000. Revenue pays this directly to the property developer on their behalf at drawdown.

Self-Build Properties

The HTB also applies to self-build properties. The same 10% calculation applies, but the capped amount is 10% of the approved valuation of the completed property, not the build costs incurred. You'll need a formal valuation from an approved valuer.

For self-builds, the rebate is typically paid in stages as work progresses, rather than in a single lump sum on completion.

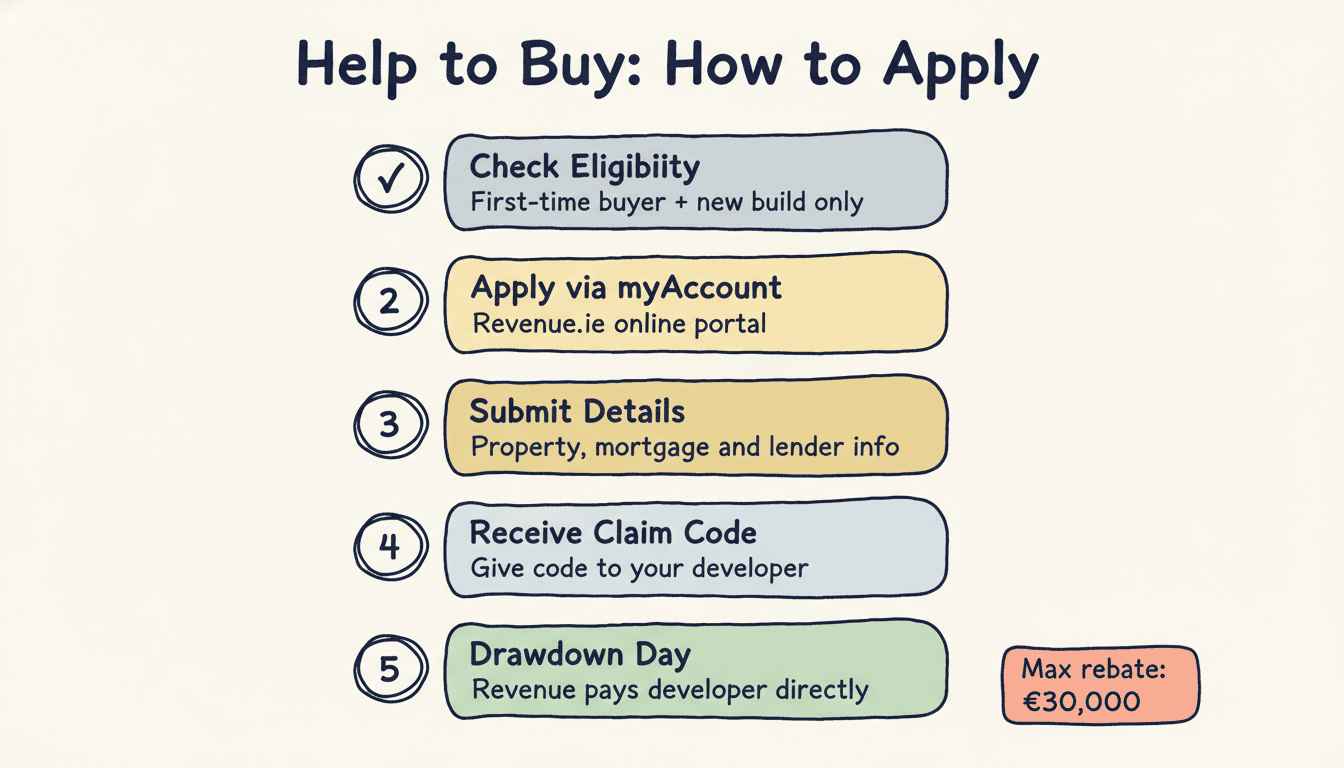

How to Apply for Help to Buy

The application process is done online through Revenue's myAccount or the Revenue Online Service (ROS).

Step 1: Create or log in to myAccount Go to myaccount.revenue.ie.

Step 2: Access the Help to Buy section Under "Manage my Tax," select "Help to Buy."

Step 3: Complete the application You'll provide:

- Details of the property (address, valuation, developer/contractor)

- Your income tax history (Revenue populates this automatically)

- Your mortgage details and lender

Step 4: Receive your HTB Claim Code Revenue issues you a unique claim code, which you give to your developer. The developer logs in to verify and approve the claim.

Step 5: Drawdown When you draw down your mortgage, Revenue releases the rebate directly to the developer as part of your deposit arrangement.

Revenue's Help to Buy guidance has the definitive process and current approved contractor list.

How Does HTB Interact With the First Home Scheme?

The First Home Scheme (FHS) is a separate, complementary initiative run by the Housing Agency and the NTMA. Where your mortgage + HTB rebate doesn't bridge the gap to the purchase price, the FHS can provide an additional equity stake (effectively a top-up loan) of up to 30% of the market value, subject to maximums.

HTB and the FHS can be used together. HTB provides a cash rebate from Revenue; FHS provides a government equity stake that you repay later (or pay interest on). Revenue has no role in the FHS — it's administered separately.

Frequently Asked Questions

Can I use the HTB on an apartment? Yes. New-build apartments qualify for HTB, provided the purchase price is €500,000 or less and all other conditions are met.

I've been living abroad. Do my foreign earnings qualify for the four-year tax history? Only Irish income tax (and DIRT) counts toward the HTB rebate. Tax paid to foreign authorities does not qualify. If you've been working abroad and returned to Ireland recently, your available rebate may be limited.

What if I pull out of the purchase after claiming? If you receive an HTB rebate but do not complete the purchase, you are obliged to repay it to Revenue. Revenue tracks completion through the developer portal. Failure to repay is a serious tax compliance matter.

Does the five-year residency requirement affect stamp duty? If you sell or rent out the home within five years, Revenue may claw back the HTB rebate proportionally. This is known as the "clawback period." Always factor this into your planning if you think you might need to sell within five years.

I'm buying jointly with a sibling who has previously owned a home. Can I use HTB? No. All purchasers named on the mortgage must be first-time buyers. If one co-buyer has previously owned a property, the HTB is not available for that purchase.

This article is for informational and estimation purposes only. It does not constitute professional tax advice. Tax rules can change. Always check Revenue.ie for the latest figures or consult a qualified tax advisor for your specific situation.

Written by a Chartered Accountant

All guides on Irish Tax Estimator are written and reviewed by a qualified Irish Chartered Accountant to ensure accuracy. This article is for general information only and does not constitute professional tax advice.

Share this guide