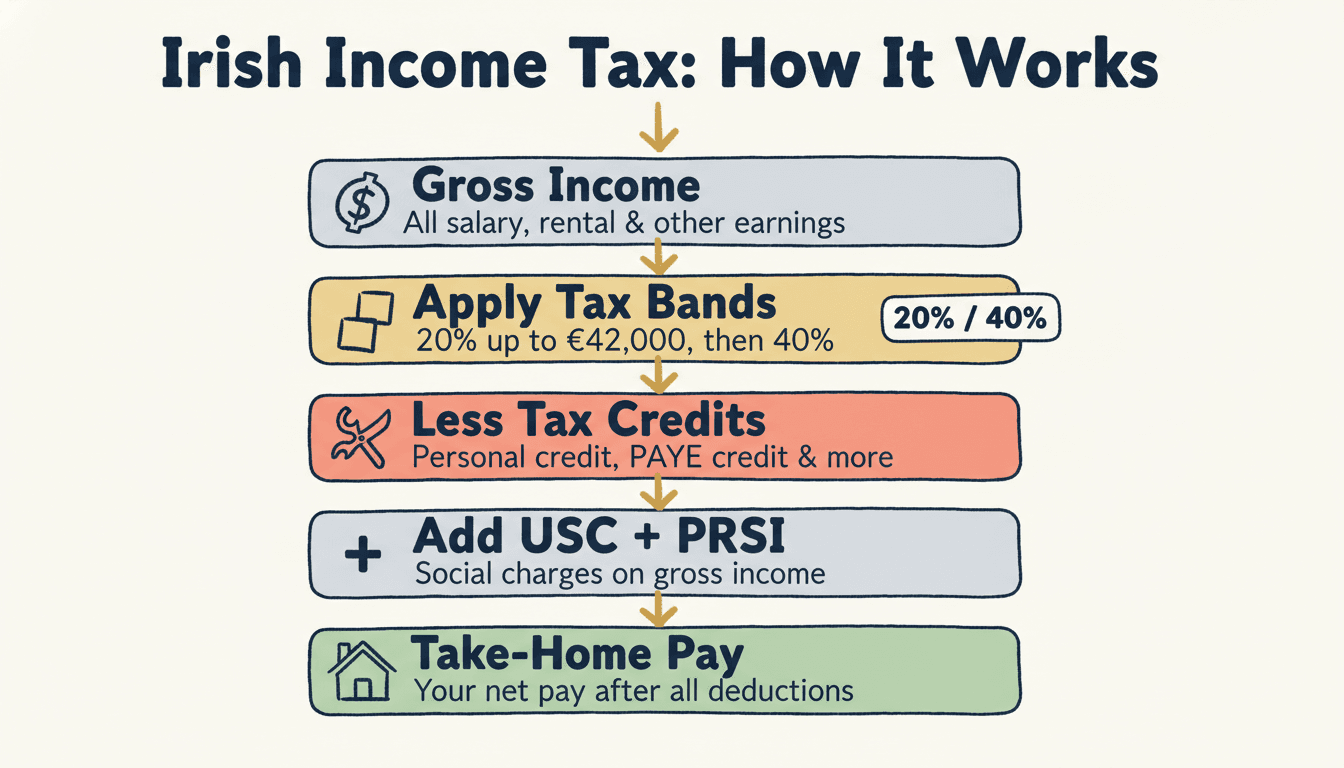

- Ireland deducts three separate charges from your salary: Income Tax, USC, and PRSI

- Income Tax uses two rates — 20% on the first €44,000 and 40% above that — but tax credits reduce the actual amount you pay

- On a €50,000 PAYE salary in 2025, a single person takes home roughly €39,700 after all deductions

Understanding your tax bill in Ireland can feel complicated, but the core structure is actually straightforward once you break it down. In this guide I'll walk through exactly how income tax is calculated step by step — using a real example of a €50,000 PAYE salary.

The Three Deductions on Your Payslip

When you earn a salary in Ireland, three separate charges are deducted before you receive your take-home pay:

- Income Tax — the main tax on your earnings

- USC (Universal Social Charge) — an additional charge introduced in 2011

- PRSI (Pay Related Social Insurance) — funds social welfare and pensions

Let's look at each one in detail.

1. Income Tax

The Two Rates

Ireland uses a two-rate income tax system:

| Rate | Applies to |

|---|---|

| 20% (Standard Rate) | First €44,000 of income (single person, 2025) |

| 40% (Higher Rate) | Anything above €44,000 |

For married couples with one income, the standard rate band extends to €53,000.

Tax Credits — The Key to Reducing Your Bill

Before you actually pay income tax, you subtract your tax credits. These are fixed amounts that reduce your tax liability euro-for-euro. In 2025, a single PAYE employee receives:

| Credit | Amount |

|---|---|

| Personal Tax Credit | €2,000 |

| PAYE Tax Credit | €2,000 |

| Total | €4,000 |

This means you'd need to owe more than €4,000 in income tax before you actually pay anything — so the first €20,000 of a single PAYE worker's income is effectively income-tax-free. Married couples may also be eligible for additional credits — such as the Home Carer Tax Credit (worth €1,950 for qualifying couples) — which reduce the bill further.

2. USC (Universal Social Charge)

USC applies to gross income above €13,000. Incomes at or below €13,000 are fully exempt.

| Band | Rate |

|---|---|

| First €12,012 | 0.5% |

| €12,013 – €27,382 | 2% |

| €27,383 – €70,044 | 3% |

| Above €70,044 | 8% |

USC is charged on your gross salary — pension contributions do not reduce your USC.

3. PRSI

Most PAYE employees pay Class A PRSI at 4.1% on all earnings (the exemption applies only below €352/week, roughly €18,304 per year). Under the multi-year PRSI roadmap, the rate rises to 4.2% from 1 October 2025 — so the blended rate across the 2025 tax year is about 4.125%.

Self-employed individuals pay Class S PRSI at the same rates, with a minimum annual payment of €650.

Worked Example: €50,000 Salary, Single PAYE Employee

Let's calculate the full tax for a single person earning €50,000 per year.

Income Tax

| Calculation | Amount |

|---|---|

| First €44,000 × 20% | €8,800 |

| Remaining €6,000 × 40% | €2,400 |

| Gross income tax | €11,200 |

| Less: Personal Tax Credit | –€2,000 |

| Less: PAYE Tax Credit | –€2,000 |

| Net Income Tax | €7,200 |

USC

| Band | Calculation | Amount |

|---|---|---|

| €0 – €12,012 | × 0.5% | €60.06 |

| €12,013 – €27,382 | × 2% | €307.40 |

| €27,383 – €50,000 | × 3% | €678.54 |

| Total USC | €1,046.00 |

PRSI

€50,000 × 4.125% (blended 2025 rate) = €2,063

Summary

| Annual | Monthly | Weekly | |

|---|---|---|---|

| Gross Salary | €50,000 | €4,167 | €962 |

| Income Tax | –€7,200 | –€600 | –€138 |

| USC | –€1,046 | –€87 | –€20 |

| PRSI | –€2,063 | –€172 | –€40 |

| Take-Home | €39,691 | €3,308 | €763 |

Effective tax rate: 20.6%

Marginal tax rate: ~47% (income tax 40% + USC 3% + PRSI 4.1% on the next euro earned). The often-quoted 52% marginal rate only applies once income passes €70,044, where USC jumps to 8%.

Key Takeaways

- The 40% rate only applies to income above the standard rate band — not your entire salary

- Tax credits reduce your bill significantly — always make sure you're claiming all credits you're entitled to

- USC is a separate charge on top of income tax — many people confuse the two

- Your marginal rate (what you pay on the next euro earned) is higher than your effective rate (what you actually pay overall)

Use the Irish Tax Estimator calculator to see your exact figures based on your salary, employment type, and personal circumstances.

This article is for general information only and does not constitute professional tax advice. Figures are based on Revenue.ie guidelines for tax year 2025. Consult a qualified tax advisor for advice specific to your situation.

Written by a Chartered Accountant

All guides on Irish Tax Estimator are written and reviewed by a qualified Irish Chartered Accountant to ensure accuracy. This article is for general information only and does not constitute professional tax advice.

Share this guide