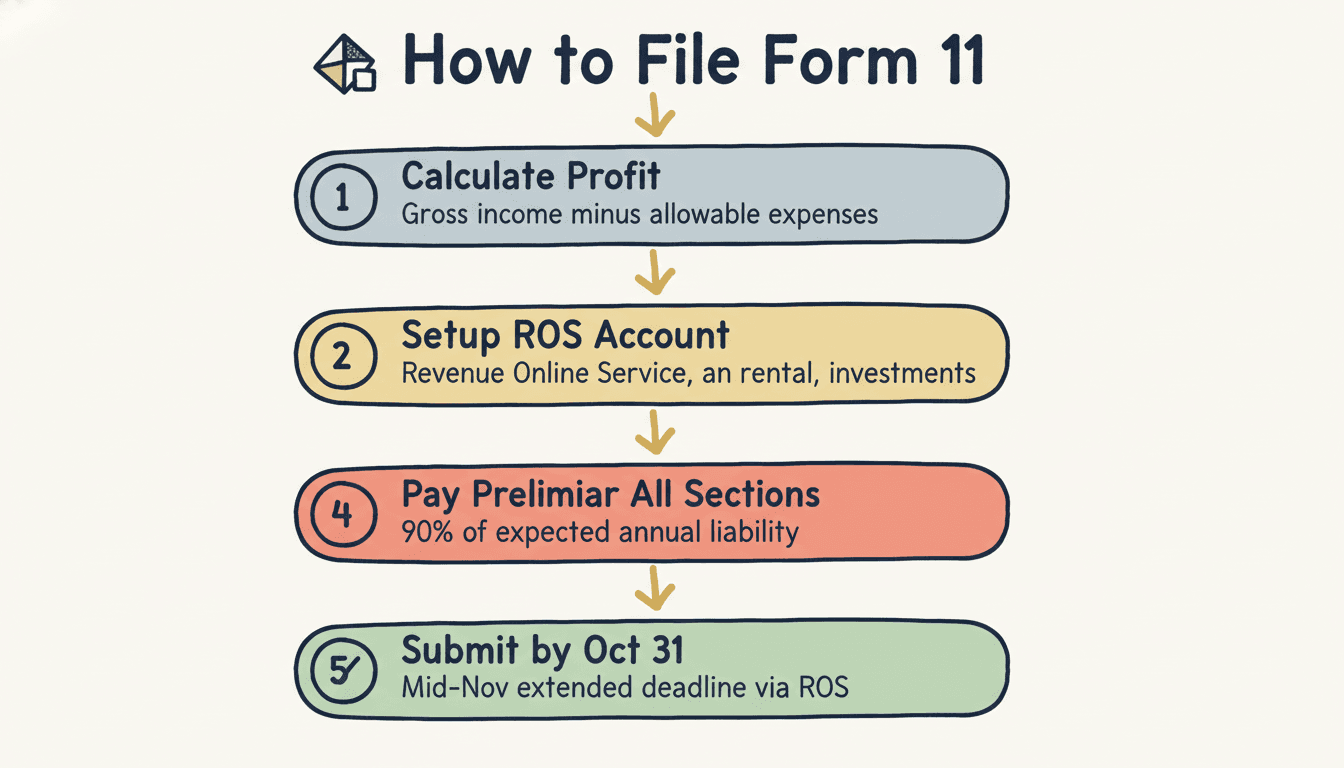

- Self-employed people and those with non-PAYE income over €5,000 must file a Form 11 by 31 October each year (or mid-November via ROS online)

- Preliminary tax — an advance payment equal to 90% of your expected tax bill — must be paid by the same deadline

- Filing late triggers a 5–10% surcharge on top of your tax bill; missing the payment deadline adds daily interest at 0.0219%

The Form 11 is Ireland's annual income tax return for self-assessed taxpayers — the self-employed, company directors, landlords, and PAYE workers with significant side income or capital gains. If you've recently gone freelance, started a business, or taken on rental income, you need to file this form every October. This guide walks through exactly what's required, what common mistakes to avoid, and how the whole process works.

Who Needs to File a Form 11?

You must file a Form 11 if:

- You are self-employed (sole trader, freelancer, contractor) with income from a trade or profession

- You are a company director with income from the company (other than PAYE salary where all tax is deducted at source)

- You have rental income from a property

- You have investment income — dividends, foreign income, or returns from ETFs/funds

- You have non-PAYE income exceeding €5,000 per year (including freelance, side hustle, commission)

- You have capital gains (from shares, property, crypto, etc.)

- You have income from abroad on which Irish tax is due

PAYE workers whose total income is below €5,000 outside of PAYE can use the simpler Form 12 or claim/adjust through myAccount instead.

The Key Dates You Cannot Miss

| Date | Obligation |

|---|---|

| 31 October 2025 | Form 11 filing deadline (paper) and preliminary tax payment for 2025 |

| Mid-November 2025 | Extended deadline for filing AND paying via Revenue Online Service (ROS) |

| 31 October 2026 | Final tax balance for 2025 due (when you file the 2025 Form 11) |

What is preliminary tax? Each year you must estimate your upcoming tax liability and pay at least 90% of it in advance, by 31 October. This is called "preliminary tax" and it's essentially a deposit against your final bill. When you file your Form 11 the following October and calculate your actual liability, you either:

- Pay the remaining balance, or

- Receive a refund if you overpaid preliminary tax

Failure to pay sufficient preliminary tax by 31 October results in interest charges at 0.0219% per day on the underpaid amount.

What's Included in the Form 11?

The Form 11 is a comprehensive return that covers:

- Trade income (profit from your business or profession)

- Employment income (any PAYE salary, confirmed against P60 / payslip)

- Rental income and expenses

- Dividend and investment income

- Foreign income

- Capital gains (shares, property, crypto)

- Tax credits and reliefs (pension contributions, medical expenses, remote working, etc.)

- USC and PRSI calculations

- Details of income of your spouse (if jointly assessed)

You can file on paper (Form 11 PDF available from Revenue.ie) or online through ROS (Revenue Online Service). Online filing has a later deadline and is strongly recommended.

Setting Up ROS

ROS is Revenue's online system for self-assessed taxpayers. If you haven't used it before:

- Register for ROS at ros.ie — you'll need your PPS number and Tax Reference Number

- Revenue posts you a Digital Certificate in the mail (takes a few days)

- Install the certificate on your browser

- You can then file and pay online

The ROS extended deadline (typically around 14 November) only applies if both your return and payment are submitted through ROS. Paying by cheque or bank draft but filing online does not qualify for the extension.

How to Calculate Your Trading Profit

For self-employed individuals, the trading profit is your gross income less allowable business expenses. You pay income tax on the profit, not the turnover.

Revenue allows deductions for:

- Wages and salaries (including your own if you're a company director, but not if you're a sole trader — sole traders pay themselves out of profit, not as a deduction)

- Materials and stock

- Rent for business premises

- Professional subscriptions and insurance

- Accountant and legal fees

- Equipment (capital allowances — typically 12.5% per year over 8 years for most plant and machinery)

- Motor expenses (business proportion only)

- Travel expenses (to client sites, not commuting)

- Telephone and broadband (business proportion)

Revenue does NOT allow deductions for:

- Personal drawings (sole trader)

- Private motoring

- Entertainment

- Fines and penalties

- Capital expenditure (except via capital allowances)

Keeping clear books throughout the year — using accounting software like Xero, Surf Accounts, or even a clean spreadsheet — makes the Form 11 calculation straightforward.

Worked Example: Freelance Designer, 2025

Niall, freelance graphic designer, 2025

| Amount | |

|---|---|

| Gross invoiced income | €62,000 |

| Less materials and software | –€3,200 |

| Less professional indemnity insurance | –€800 |

| Less accountant fee | –€600 |

| Less phone (80% business) | –€360 |

| Less broadband (30% business) | –€180 |

| Less capital allowances (laptop at 12.5%) | –€125 |

| Taxable profit | €56,735 |

Tax calculation:

| Amount | |

|---|---|

| Income tax: €44,000 @ 20% | €8,800 |

| Income tax: €12,735 @ 40% | €5,094 |

| Less personal credit | –€2,000 |

| Less earned income credit | –€2,000 |

| Income tax payable | €9,894 |

| USC on €56,735 (0.5% / 2% / 3% bands, 2025) | ~€1,248 |

| PRSI Class S (blended 4.125% for 2025) | €2,340 |

| Total tax liability | ~€13,482 |

Niall's preliminary tax payment due by 31 October 2025 must be at least 90% × €13,482 = €12,134.

Use the Irish Tax Estimator income tax calculator to estimate your own liability.

Common Form 11 Mistakes to Avoid

-

Forgetting preliminary tax — The payment is due at the same time as filing. Missing it means daily interest immediately.

-

Not claiming all expenses — Many self-employed people underclaim because they're unsure what's allowed. Keep every business receipt, log mileage, and claim the allowable proportion of home office costs.

-

Forgetting to declare all income sources — Revenue cross-references with banks, platforms, and PAYE records. Omitting rental income or investment returns is a compliance risk.

-

Missing the pension top-up window — You can make a prior-year pension contribution and claim relief on this year's Form 11. The contribution must be made before 31 October. See the Irish Tax Estimator pension guide.

-

Calculating surcharges incorrectly — If you've missed a filing deadline, the surcharge is 5% of additional tax (max €12,695) within two months, and 10% (max €63,485) after two months. Include this correctly to avoid secondary issues.

Frequently Asked Questions

Do I need an accountant to file a Form 11? Not legally. Many self-employed individuals file their own Form 11 through ROS. However, if your affairs are complex (rental income, capital gains, mixed PAYE and self-employment), an accountant can ensure you claim all reliefs and avoid errors. The accountant fee is itself tax-deductible.

I only became self-employed this year. When is my first Form 11 due? Your first Form 11 covers the year you started trading. If you started in 2025, the first return is due by 31 October 2026 (covering the 2025 tax year). Importantly, you must also pay preliminary tax for 2025 by 31 October 2025, even in your first year — though new businesses can use a different method to calculate preliminary tax in year one.

What if I can't pay the full amount on time? File on time regardless. Interest accrues on late payments, but the filing surcharge (5–10%) is far worse than interest. File on time, pay what you can, and Revenue will apply interest to the balance. Revenue also has a phased payment arrangement (PPA) process for people with genuine difficulty.

How long should I keep my business records? Revenue can audit up to six years back in normal circumstances and further if fraud is suspected. Keep all business records, receipts, bank statements, and invoices for at least six years from the end of the relevant tax year.

Can I file through myAccount or do I need ROS? If your non-PAYE income is below €5,000, you can use myAccount. Above €5,000 (which means you need to file a Form 11), you must use ROS.

This article is for informational and estimation purposes only. It does not constitute professional tax advice. Tax rules can change. Always check Revenue.ie for the latest figures or consult a qualified tax advisor for your specific situation.

Written by a Chartered Accountant

All guides on Irish Tax Estimator are written and reviewed by a qualified Irish Chartered Accountant to ensure accuracy. This article is for general information only and does not constitute professional tax advice.

Share this guide